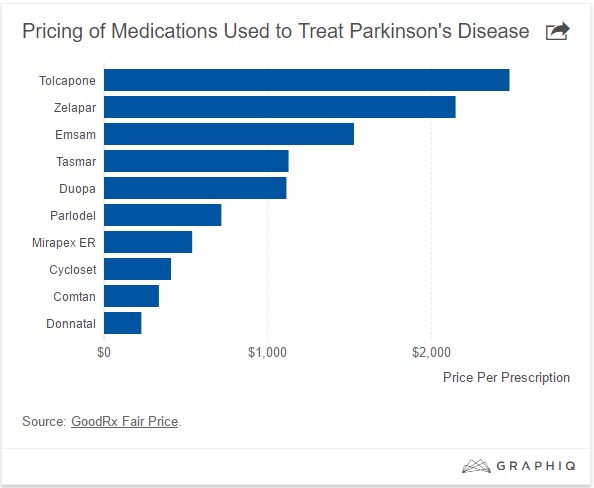

|

| [Click to Enlarge] |

Doug Long, vice president, industry relations for IMS Health, kicked off Thursday morning, April 21, at the Academy of Managed Care & Specialty Pharmacy Annual Meeting 2016, with his presentation on marketplace trends, “Charting the Course for Change: Industry Update.”

The news is not good: U.S. spending on drugs increased 12.2% to $424.8 billion in 2015, spiking 46 billion over the past year due to higher brand spending and fewer patent expirations; however, spending on brands without exclusivity reduced growth by $14.2 billion in 2015.

On the positive side, net price growth slowed in 2015 to 2.8% as concessions from manufacturers rose sharply. Other metrics from 2015 include: Brands accounted for 11% of prescriptions but drove 73% of sales; prescriptions rose 1% in the last 12 months; diabetes, autoimmune diseases, hepatitis and oncology led the spending growth; specialty new brands continued to spur growth (up 21.5%); and Abilify, Celebrex and Nexium lost patent protection.

Long looked back at 2015 and pointed out the most notable events, which included exclusive launches and price wars for hepatitis C, the arrival of the first biosimilar, Zarxio, and of generic Nexium, rescheduling of controlled substances, the unforgettable price gouging by Valeant and Turing, and merger mania extending into 2016.

As far as specialty goes, 2015 brought more innovation to hepatitis C, along with the emergence of PD1s, PCSK9 inhibitors, orphan drugs, generic Copaxone and more orals, more copayment program cooperation by payers, the patient as payer and more value-driven metrics.

Long predicted that 2016 will continue along the same path with another biosimilar approved, a CMS ruling on Part B reimbursement, a new hepatitis entrant from Merck, new FDA/DEA guidelines on controlled substances, price discussions on orphan drugs and gene therapies and a more-crowded specialty space.

Long said that total prescriptions at chains are expected to far exceed market growth, while mail-order, long-term care and independent pharmacies are going to continue to decline through 2020, at which time, chains could consume a 45.8% share of the market.

By Mari Edlin