RFP season is in full swing and a little later than usual for obvious reasons. It’s mind-boggling what PBMs are asked to do in some of these RFPs. The responses we provide are sophisticated. Isn’t it reasonable to then expect that the evaluation of those responses be equally sophisticated? If I were a plan sponsor here are the seven things I would be asking of PBMs during an RFP.

1. PBM Contract. Do you know why spreadsheeting PBM pricing offers is held in such high regard? Business math is easy 2 + 2 = 4. PBM contract evaluation isn’t so easy so decision-makers hand it off to the corporate attorney who can’t tell you the difference between ASP and WAC. I’m not suggesting the corporate attorney isn’t smart. Of course they are smart but that doesn’t mean diddly squat unless you have a trained-eye for pharmacy benefits. The problem for plan sponsors who wait until the last minute to address contract nomenclature is that it is the most important factor in determining whether your plan overpays or pays a fair price for PBM services. In PBM contracts 2 + 2 ≠ 4. Discount and rebate guarantees mean less when contract nomenclature is ambiguous.

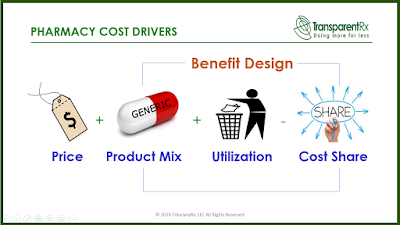

2. Benefit Design. Never once during hundreds of RFPs has any consultant or broker ever asked us for a completed benefit design as part of our response. I’ve not taken a poll so I don’t know the reason. Maybe it is because some believe benefit design doesn’t have a big role in determining cost. If that is the case, nothing could be further from the truth. Don’t put 50 questions in a RFP around benefit design where important details get lost in translation…geesh. I would be asking for a benefit design to be submitted as if we were going live with it. In pharmacy cost drivers, price is 1A and benefit design is 1B. Aside from copayments and deductibles (cost sharing) most plan sponsors know little else about their benefit design and have left it up to the PBM to decide. When the PBM is non-fiduciary that could lead to significant overpayments.

3. References. 2-3 companies who can verify the PBM’s claims (i.e. retail network, mail and specialty access and transparency) about performance. This could also include inquiries about account management and member support performance.

4. Questionnaire. 20 – 25 verifiable questions pertinent to my company’s needs. Here is where you inquire about security, reporting, disease management, MTM or alternate funding programs.

5. PBM Reverse Auction. Two PBM reverse auctions in the same competitive bidding process in fact. The first round is conducted after the claims repricing is submitted. The second round is completed after all contract concessions have been made and the resulting contracts memorialized. Usually you are down to 3-5 candidates at this point. Keep in mind that in a well run and organized reverse auction prices only go down.

6. Finalist Presentation or Interview. Don’t allow PBMs to turn it into a marketing contest. Use the time to win more contract concessions and clear up any lingering concerns.

7. Claims Repricing. Not for the purpose of determing who has the better price but to make sure the PBM is in the ballpark of the market. Claims repricings tell you what happened in the past. Claims repricings can’t tell the story of what is going to happen in the future. The PBM contract and benefit design are better suited to help predict future performance. Furthermore, if the incumbent PBM has leveraged bad product mix or poor utilization to generate its management fee you are asking PBMs in the bidding process to reprice those same bad claims.

Now score each of the six areas (excluding repricing). Here are some weights I recommend applying to each score:

Contract – 40%

Benefit Design – 25%

References – 10%

Questionnaire – 5%

Reverse Auction – 15%

Finalist Presentation – 5%

As you can see the repricing has earned no weight. The claims repricing serves to show only if the pricing is competitive nothing more. The reverse auction will establish pricing guarantees and the contract will help determine whose pricing is the most transparent. It takes time to get really good at any of these areas. Don’t give up on them the first or even second time around.

The best proponent of radical transparency and lowest net Rx cost is informed and sophisticated purchasers of PBM services. I’m not talking about 1400 SAT or 4.0 GPA sophistication. I’m referring to a high level of sophistication in the PBM arena. If it isn’t your bag don’t carry it. Find someone else who specializes to do the heavy lifting for you.